Payment Processing & Gateway Solutions

The Problem

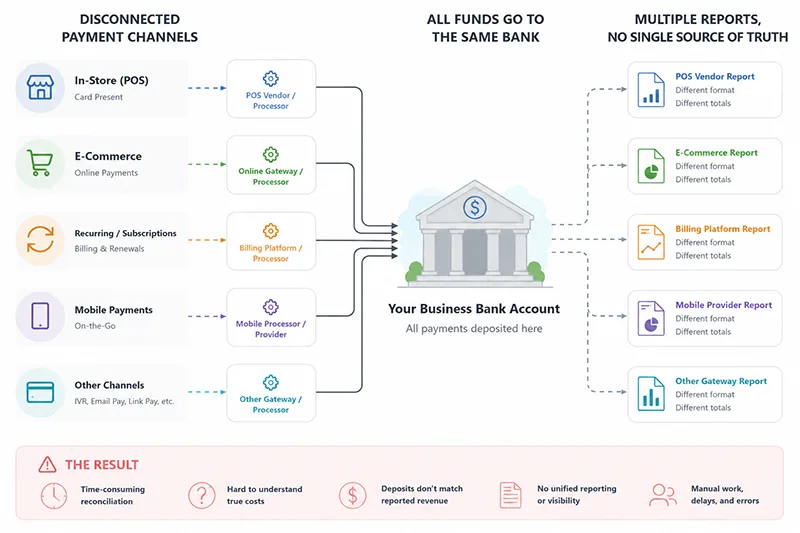

Most businesses today accept payments across multiple channels—such as in-store, e-commerce, and subscription or recurring billing—often supported by different vendors and technologies that were never designed to function as a single system.

The result is a set of common, but often overlooked, problems:

- You’re not entirely sure what you’re paying in processing fees—or how those costs are calculated

- You rely on multiple providers (processor, gateway, POS, integrations), with no single point of accountability

- Different vendors apply different rates and pricing structures, making it difficult to understand your true cost

- Deposits don’t clearly match reported revenue, making reconciliation more difficult than it should be

- In-store and online payments are tracked separately, with no unified reporting

- Staff spend time manually reconciling transactions across systems

- Payment data doesn’t flow cleanly into your accounting or reporting tools

- Lack of integration forces payments to be handled manually, creating delays and increasing risk of error

- Adding new capabilities introduces more complexity instead of simplifying operations

What should be a straightforward part of running a business—accepting and tracking payments—becomes fragmented, time-consuming, and harder to manage as you grow, to the point where more effort is spent managing payments than delivering the products or services those payments are for.

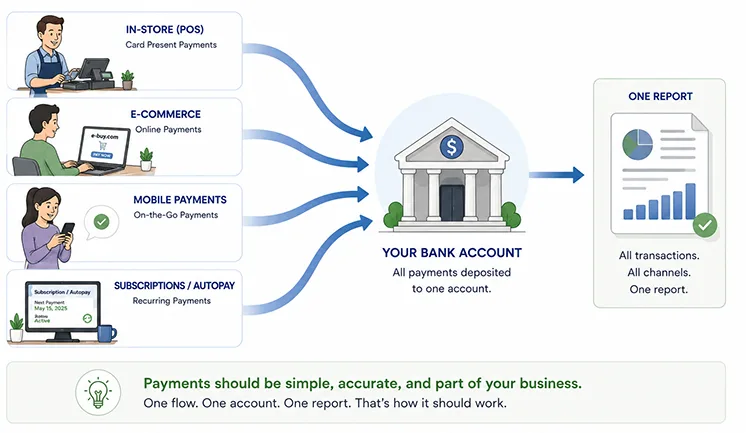

How It Should Work

Most businesses already have a sense of how this should work—they just haven’t seen it implemented this way, or had it presented to them.

- Payment processing shouldn’t feel complicated or disconnected from the rest of your business

- A single provider should support all payment channels—POS, e-commerce, and subscriptions—with one pricing structure, one report, and one monthly fee

- Deposits should match transactions and be delivered the next business day

- Payment terminals should integrate directly into your existing systems, including customized software solutions, minimizing or eliminating manual transaction handling

Payments should operate as part of your business—not as a separate system you have to manage.

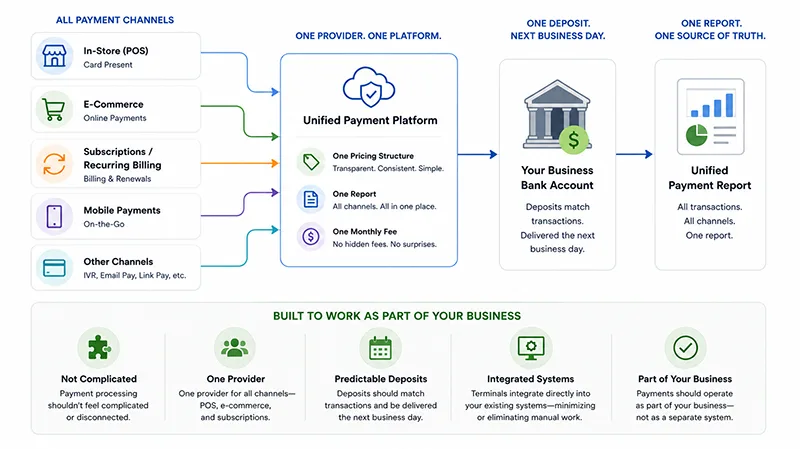

How Harrison Consulting Solves the Problem

Harrison Consulting delivers a unified payment system by combining processing, integration, and reporting into a single, cohesive solution. Instead of managing multiple vendors and disconnected tools, your payments operate as part of a consistent, well-structured system.

High-Impact Pricing

We provide access to a transparent, interchange-plus pricing model:

Interchange + 0.15% + $0.05 per transaction

This structure removes bundled pricing and hidden markups—giving you clear, predictable costs that scale efficiently with your business.

For context, many flat-rate processors charge around 2.9% + $0.30 per transaction, regardless of card type. Interchange-based pricing reflects actual costs, which are often significantly lower.

Flexible Terminal & System Integration

We support modern, PCI-compliant payment terminals—including Clover and Ingenico devices—that integrate directly into your existing POS systems or custom software.

Ingenico Link/2500

Compact wireless terminal

Clover Flex 4

Handheld smart POS

Clover Mini

Compact full POS

Clover Station

Full countertop system

Transactions can be initiated and processed within your systems, minimizing or eliminating manual handling and reducing operational friction.

Secure Tokenization

Our platform supports secure card tokenization, allowing customers to safely reuse payment methods for future purchases and subscriptions without exposing sensitive data.

Clean Deposits & Cash Flow

Full transaction amounts are deposited the next business day, with fees handled separately in a consolidated monthly statement—providing clarity and simplifying accounting.

One System. All Payment Channels.

In-store, online, mobile, and recurring payments all flow through a single system—one merchant account, one report, and one source of truth.

Pricing Details

Most payment providers use one of two pricing models: flat-rate pricing or interchange-plus pricing.

Flat-rate pricing (for example, 2.9% + $0.30 per transaction) bundles all costs into a single number. While this approach is simple to understand, it often hides the true cost of processing and can result in higher fees— especially for debit transactions or lower-risk payments.

Interchange-plus pricing takes a different approach. It separates the actual cost of the transaction from the provider’s fee. Instead of a bundled rate, you pay the true underlying cost (interchange) plus a clearly defined, consistent margin. This model provides transparency and, in most cases, results in lower overall processing costs.

That said, interchange-plus pricing does include standard industry fees—such as monthly platform fees, PCI compliance, and administrative costs—which typically total around $500 per year.

For very low transaction volume, flat-rate pricing can sometimes be the more economical choice due to its lack of fixed costs. However, as transaction volume increases, the cost difference becomes significant.

So, what is Interchange?

Interchange is the base cost of every card transaction. It is set by the card networks and paid directly to the cardholder’s issuing bank. Every processor—regardless of provider—pays this same cost.

What makes interchange complex is that it isn’t fixed. It varies depending on the type of card being used (debit vs. credit), whether the card includes rewards (cash back, points), how the transaction is processed (in-person vs. online), and the level of security and verification applied.

Because of this, each transaction carries a slightly different cost. Interchange is not markup—it is the actual cost of moving money through the card networks.

Once you understand interchange, pricing becomes straightforward.

What Does This Look Like Over a Year?

Example: One $200 transaction per day (≈ $73,000 annually)

Interchange-Plus

Per Transaction: $2.10

Annual Processing: $766.50

Estimated Annual Fees: ~$500

Total Annual Cost:

$1,266.50

Transparent pricing based on true interchange cost plus a fixed margin.

Flat-Rate Pricing

Per Transaction: $6.10

Annual Processing: $2,226.50

Annual Fees: Included

Total Annual Cost:

$2,226.50

Simple pricing, but typically higher overall cost as volume increases.

See What Your Payment System Should Look Like

If your current setup feels more complicated than it should be, we can help you simplify it—while reducing costs and improving visibility.

Let’s build what your business needs next